Economic efficiency of accounts receivable factoring example. Factoring as a form of business lending in Russia using the example of Factoring Company Life LLC

As already noted, factoring operations are directly related to accounts receivable.

The “current assets” section of the balance sheet reflects short-term receivables (with a maturity of up to 12 months) and long-term (with a maturity of more than 12 months). At the same time, for each type of debt, the debt of the participants (founders) for contributions to the authorized capital, advances issued, and other debtors is identified. At the same time, accounts receivable management is an important area.

Effective accounts receivable management serves several purposes.

First, receiving payments from debtors is one of the company's main sources of cash. Consequently, the organization of optimal modes of movement of receivables directly affects the goal of the enterprise in market conditions - generating income and profit.

Secondly, in modern conditions there are certain contradictions between procurement policies and sales policies, which gives additional importance to the implementation of effective collection procedures (in this case, the receipt or collection of funds by an enterprise from its debtors).

Thirdly, as practice shows, taking into account the real costs or benefits of credit decisions made (in particular, from providing buyers with the right to defer payment) can be used as a tool to expand sales and increase the turnover of current assets.

Three areas of accounts receivable analysis can be distinguished: analysis of the total amount of accounts receivable by the timing of its occurrence; debtor analysis; debt analysis by product range.

Very often situations arise when debtors do not pay their debts. Then they have to be written off as bad debts. This brings losses to the company.

A similar situation developed at OJSC Svyaz. The company has been operating on the market for more than 10 years and receives a fairly stable profit.

OJSC Svyaz actively uses factoring to ensure the return of funds from debtors.

The use of factoring operations allows OJSC Svyaz to solve the problem of non-payments through the timeliness and efficiency of settlements between the supplier and the buyer through an intermediary - a factoring company or bank.

The effectiveness of the use of factoring operations in settlements between the supplier and the buyer for the supplied products of Svyaz OJSC.

Table 1 shows that as a result of using factoring, OJSC Svyaz receives an economic effect in the amount of 9,210 rubles.

Table 1 - Calculation of the efficiency of factoring in OJSC Svyaz

|

Indicators |

Amount, rub. |

|

|

A. Without using factoring: partial payment for products has been made buyer's balance total loss adjusted for inflation |

|

|

|

B. Using factoring: Products have been shipped to the buyer 85% of the payment amount was received from the factor firm the calculation has been made in full (subject to demand payment from the buyer) losses from inflation (at 1% per month) payment for factor firm services (3% of the transaction amount) total amount of expenses and losses adjusted for inflation |

|

|

|

Economic effect provided that factoring is used |

Thus, the effectiveness of factoring can be assessed by comparing the indicators of accounts receivable before the use of factoring and after its implementation. As a rule, the results are better when factoring is used.

The supplier, participating in a factoring operation, has the opportunity to speed up the receipt of money into its account and pay suppliers without delay, which helps speed up settlements and reduce the level of overdue debt.

3. Analysis of the effectiveness of attracting factoring operations

3.1 Methodological aspects of assessing the effectiveness of factoring

Let's consider the effectiveness of factoring for its various participants using a specific example.

As already noted, factoring operations are directly related to accounts receivable.

In the “current assets” section of the balance sheet of domestic enterprises, in accordance with current legislation, both current receivables (with a maturity of up to 12 months) and non-current (with a maturity of more than 12 months) are shown. At the same time, for each type of debt, the debt of the participants (founders) for contributions to the authorized capital, advances issued, and other debtors is identified. At the same time, accounts receivable management is an important area of work for the financial and accounting services of an enterprise.

Its implementation has several goals. Firstly, receiving payments from debtors is one of the main sources of cash flow for an enterprise. Consequently, the organization of optimal modes of movement of receivables directly affects the goal of the enterprise in market conditions - generating income and profit. Secondly, in modern conditions there are certain contradictions between procurement policies and sales policies, which gives additional importance to the implementation of effective collection procedures (in this case, the receipt or collection of funds by an enterprise from its debtors). Thirdly, as practice shows, taking into account the real costs or benefits of credit decisions made (in particular, from providing buyers with the right to defer payment) can be used as a tool to expand sales and increase the turnover of current assets.

Three areas of accounts receivable analysis can be distinguished: analysis of the total amount of accounts receivable by the timing of its occurrence; debtor analysis; debt analysis by product range.

Very often situations arise when debtors do not pay their debts. Then they have to be written off as bad debts. This brings losses to the company.

A similar situation developed at JSC Triton. This organization has been operating on the market for 8 years and receives a fairly stable profit. The organization is engaged in wholesale and retail trade, so accounts receivable are a common occurrence for it. In order to protect itself, the organization assesses the reliability of customers.

Published company ratings, analysis of financial statements of potential buyers, determination of risk indices, and other methods of assessing buyers help solve this problem. When assessing a client’s reliability, it is also useful to use the entire arsenal of tools used by credit institutions. The organization CJSC Triton maintains a file of its main consumers, providing certain rules for classifying them according to the degree of reliability. The development of such dossiers and methods for assessing customer reliability became the subject of a social organizational project, within the framework of which a rating assessment of customer reliability was identified. For this purpose, the composition of indicators characterizing the solvency and financial stability of the analyzed enterprises was determined. Table 3.1 shows a set of indicators used by Triton JSC.

Indicator 1 of Table 3.1 - non-payments - characterizes the solvency of the enterprise on the day of drawing up the balance sheet. To determine it, data on the financial statements of the analyzed enterprise (information on overdue loans), operational data from the bank on delays in the payment of wages to employees, tax payments, and payment of bills to suppliers and contractors are used.

Table 3.1 – Preliminary assessment of the solvency and financial stability of the enterprise

|

Index |

Calculation method |

|

1. Non-payments (delays on loans, taxes, payment of supplier bills, other obligations) |

Data from the balance sheet and financial statements of an enterprise. Information from the bank where the company provides cash and settlement services. Information from other sources of information |

|

2. Independence coefficient, % |

The ratio of equity (1st section of liabilities), multiplied by 100%, to the balance sheet currency |

|

3. Financial stability coefficient, % |

The ratio of the amount of equity and long-term loans, multiplied by 100%, to the balance sheet currency |

|

4. Business activity coefficient, % |

The ratio of sales revenue, multiplied by 100%, to the balance sheet currency |

|

5. Enterprise efficiency ratio, % |

Ratio of balance sheet profit multiplied by 100% to balance sheet currency |

|

6. Efficiency ratio of own funds, % |

Ratio of net profit (after taxes) multiplied by 100% to equity |

|

7. Profitability of the enterprise, % |

The ratio of the efficiency ratio of own funds, multiplied by 100%, to the average yield of securities, % |

|

8. Total coverage ratio for the balance, % |

Ratio of current assets (2nd section of assets), multiplied by 100%, to short-term liabilities |

Indicator 2 determines the share of the enterprise's owners (shareholders) in the total value of the enterprise's property. If this figure is above 50%, then the risk of creditors is minimized. After all, relatively speaking, by selling half of its property, formed from its own funds, an enterprise can pay off its debt obligations, even if the other half of the property (in which borrowed funds were invested) is devalued for some reason.

Particularly important is the financial stability coefficient. This coefficient shows the share in the total value of the property of all sources of funds that the enterprise can use in its current economic activities without damage to creditors. This coefficient limits the investment of short-term borrowed funds in the formation of enterprise property only to assets that are easily sold and quickly returned to cash form.

The business activity coefficient, which shows the volume of products for the production of which the enterprise’s property is used, is also very important. This coefficient depends not only on the efficiency of use of the enterprise’s property, but also on the duration of the period for which it is calculated.

The enterprise efficiency ratio allows you to determine the period of time over which the annual profit received can compensate for the cost of the enterprise's property. The efficiency ratio of own funds gives a generalized assessment of the effectiveness of investing funds; it gives a generalized assessment of the effectiveness of investing funds in a given enterprise. This indicator can always be compared with the possibility of alternative investments (for example, purchasing shares of other enterprises). Such a comparison, made in relative figures, shows the profitability of the enterprise (indicator 7). But often this indicator is impossible to calculate, since there is no data on the average percentage of income on securities.

The approximate degree of creditors' risk is determined using the overall coverage ratio on the enterprise's balance sheet (indicator 8, Table 3.1). To do this, the current assets of the enterprise are divided by the amount of short-term liabilities. The result obtained shows whether the company will be able to pay its debt obligations maturing in the current year, turning all current assets into cash. A high coverage rate can be a consequence of the influence of both positive and negative factors, which is determined by a more in-depth additional analysis.

For each of the above indicators, JSC Triton establishes a range of values. Depending on how a given indicator is “placed” in the established range, it is “assigned” a certain weight (in points). The points are then summed up. Based on the points scored, enterprises are divided into groups. Thus, JSC Triton distinguishes five classes of enterprises:

The highest category includes enterprises with an absolutely stable financial condition, which is confirmed by a high rating both in general and for individual indicators;

The first category includes enterprises whose financial condition is generally stable, but some indicators deviate slightly from the norm;

The second includes enterprises that have signs of financial tension, to overcome which the enterprise has the potential;

The third includes high-risk enterprises that are able to overcome the tension of their financial condition through restructuring, product renewal, diversification of activities, etc.;

The fourth category includes enterprises with an unsatisfactory financial situation and no prospects for its stabilization.

Since the number of buyers of the Triton CJSC organization is quite large, the organization uses a ranked list of consumer groups, assigning to each group a certain rule for guaranteeing transactions (Table 3.2).

Table 3.2 – Grouping of consumers by reliability classes

As can be seen from Table 3.2, the organization actively uses factoring in order to ensure the return of funds from debtors.

The use of one of the new forms of payment - factoring operations in the economy allows Triton CJSC to solve the problem of non-payments through the timeliness and efficiency of settlements between the supplier and the buyer through an intermediary - a factoring company or bank. The basic principle of factoring is that the factor company buys from its clients their claims for their buyers and within 2–5 days pays 70–90% of the claims in the form of an advance, and the client will receive the remaining 10–30% after he will receive an invoice from the buyer.

The effectiveness of the use of factoring operations in settlements between the supplier and the buyer for delivered products, according to Triton CJSC, is shown in the table below (Table 3.3).

Table 3.3 shows that as a result of using factoring, Triton CJSC receives an economic effect in the amount of 9,210 rubles.

Table 3.3 – Calculation of the efficiency of factoring at Triton CJSC

|

Indicators |

Amount, rub. |

|

|

A. Without using factoring: partial payment for products has been made buyer's balance total loss adjusted for inflation |

||

|

B. Using factoring: Products have been shipped to the buyer 85% of the payment amount was received from the factor firm the calculation has been made in full (subject to demand payment from the buyer) losses from inflation (at 1% per month) payment for factor firm services (3% of the transaction amount) total amount of expenses and losses adjusted for inflation |

||

|

Economic effect provided that factoring is used |

In order to strengthen settlement and payment discipline, also when concluding contracts with buyers, Triton CJSC includes in them conditions for the accrual of interest for late payments, that is, it applies the principles of commercial lending at the level of the annual refinancing rate.

So, for example, if the buyer’s debt for a period of 80 days amounted to 34,440 rubles, then after its expiration the buyer will have to pay 37,385 rubles. (2945 rubles will be the amount of accrued interest at a refinancing rate of 38%).

In settlements between enterprises, the practice of providing discounts from the contract price when reducing the terms of payment for products (works, services) is also used. This method becomes especially relevant in conditions of inflation. In this case, the effect is equal to the difference between the amount of losses from inflation and the amount of the discount from the contract price.

a commercial activity(fourth block) covers the organization... of documents. In non-traditional directions activities can be distinguished factoring, forfeiting, guarantees, storage of valuables...

Factoring as a form of business lending in Russia using the example of MFC TRUST

Thesis >> BankingLicensing currently in preparation activities commercial organizations as financial agents, ... . Varieties " Factoring- Classic": factoring with regression; factoring without recourse; factoring timely. " Factoring- Classic" ...

Aspects of study factoring as a source of financing activities enterprises) 1.1 Essence and types factoring Factoring– financial commission... for the amount of payments for factoring. Payments by factoring included in commercial expenses are the amount...

Factoring its legal regulation

Coursework >> Banking3 1. Concept factoring. 5 2. Agreement factoring. 7 2. 1. Subject of the agreement factoring. 8 2.2 Parties to the agreement factoring. 9 3. Relationships between... factoring services may involve studying commercial activities and the financial condition of the client’s debtors...

Pokamestov Ilya Evgenievich – Ph.D., Associate Professor at MESI,

General Director of FACTORing LLC (Moscow)

Lednev Mikhail Vladimirovich – Ph.D.,

Head of Marketing Department of FC POLITEX (Moscow)

Corporate Finance Management

06 (54) 2012

In recent years, the factoring market in Russia has been developing at a rapid pace, but only a small proportion of Russian companies already use this financial instrument. For most, factoring services remain largely not fully understood, and the more important it becomes for managers and financial specialists to evaluate various indicators of the effectiveness of factoring in enterprises.

According to Expert RA, at the end of the first half of 2012, there were about 35 active players in the factoring market in Russia - banks and factoring companies, or factors (as companies or banks that provide factoring services are usually called). The market leaders at the moment are large Russian banks or their subsidiaries: VTB Factoring Group of Companies (VTB Factoring LLC and Transcredit Factoring CJSC), Promsvyazbank, Alfa-Bank, Petrocommerce Bank, NFK Group of Companies (part of financial corporation "URALSIB").

In general, factoring services in the world, according to International Factors Group, are offered by approximately 2,700 companies and banks, among their clients there are about 485 thousand companies.

According to most indicators that allow us to assess the level of development of the factoring market in the country (factoring share in GDP, turnover per client, average number of clients in the country), the Russian market lags behind the rest of the world. Thus, the global share of factoring in GDP is more than 3%, in European countries it is more than 6%, and in Russia it does not exceed 1.5%.

Among the clients of factoring companies, there are several main categories:

Distribution company (trade and purchasing);

Manufacturing company;

Large trading network (retailer);

a “subsidiary” of a Western company or an international company;

Exporting company.

The main clients of the factors are companies of the first type, the majority of which are suppliers of consumer goods and food products to large retail chains. Such companies usually cannot boast of good financial condition and the presence of large assets.

Manufacturing companies that do not have their own departments for credit work with customers are often interested in protecting against the risks of non-payment of debtors, managing accounts receivable (especially in the regions), and financing cash gaps in case of overdue payments.

The next type of client that is very attractive to factors are large retail chains. Concluding a partnership agreement with a network and using a reverse factoring scheme gives the factor access to a huge number of potential clients in the form of suppliers of a given retailer.

International companies or their subsidiaries operating in the Russian Federation usually do not show interest in financing, because receive it from abroad from their parent companies. They are accustomed to a wide range of factor services that are offered to them abroad, so such clients are demanding not only in terms of the quality of services, but also in their price put forward by factors.

They are mainly interested in protection against credit risk and in assessing buyers, since they often do not know Russian specifics and cannot adequately assess credit risks, so their most popular services are non-recourse or term factoring.

Now in the Russian market, different factors put forward different requirements for their clients. By summarizing these requirements, we can create a rough description of the company that they would be willing to accept for service:

The period of actual activity is at least one year;

A form of contractual relations with debtors providing for deferred payment;

The deferment period is up to 180 days;

The client’s monthly turnover is at least 3 million rubles;

Number of debtors - from one;

Non-cash form of payment;

Lack of affiliation between supplier and debtors.

There are many quantitative and qualitative methods for assessing the performance of companies and enterprises in various fields of activity. Among them it is worth noting the following:

Functional and cost;

Extrapolation;

Comparative;

Expert.

When analyzing efficiency, one cannot ignore the features specific to a particular industry that determine the success of doing business. For the factoring market, in our opinion, this is the company’s image, length of service, experience in the market, the availability of high-quality software, including an online client module, and qualified personnel.

Let us highlight the main criteria for evaluating a supplier of factoring services from the point of view of their consumers:

Reputation, including reviews from existing clients;

Number of mentions in the press;

Years of service and experience in the market;

Volume of the portfolio of factoring transactions;

Availability of additional services in addition to financing;

Terms of service;

Availability of high-quality software, including an online client module;

Amount of commission;

Quality of the website 1.

1 Pokamestov I.E., Podlesnova A.Yu. Budgeting and business planning of factoring activities // Factoring and trade financing. – 2008. - No. 1

It is immediately worth noting that all of the above criteria can be divided into price and non-price. Developed factoring markets are characterized by high awareness among consumers of factoring services, so they pay primary attention to non-price parameters. In Russia, this trend began to appear only over the past few years, however, due to the financial crisis, and currently, most clients evaluate factors only in terms of the cost of factoring products.

To assess the effectiveness of these products on the consumer side, quantitative price indicators are used. Among them are the amount of remuneration of the factoring company, the effective interest rate, the absolute costs of using factoring, and the receivables release ratio. Quantitative indicators include, first of all, the amount of remuneration charged by the factor for its services.

The structure of the factoring commission usually looks like this.

1. One-time costs (initial):

Signing an agreement for factoring services;

Installation and configuration of software modules (for electronic factoring).

2. Fixed fee for document processing

3. A fixed percentage of the supplier’s turnover for factoring administration. Most of this part of the commission represents payment for services provided by the factor, namely:

Monitoring timely payment of goods by debtors;

Work with debtors in case of delays in payments (only for factoring without recourse);

Accounting for the current state of accounts receivable and providing the supplier with relevant reports;

Collection of payment requests.

4. Premium for risks assumed by the factor:

Risk of late payment for supplies (liquidity risk);

Risk of insolvency of debtors (credit risk);

The risk of a sharp change in the cost of credit resources (interest rate risk);

Risk of bankruptcy of the seller.

5. The cost of credit resources necessary to finance the supplier (in practice, this percentage is calculated daily, usually it is 2-396 times higher than the rates on short-term bank loans, which is associated with increased risks assumed by the factor, as well as with the availability of related services) .

In addition, the factor may charge other related fees, for example, for each day that customers are late in paying. The main types of factoring commissions, generally accepted in most factoring companies, are given in table. 1.

Table 1. Types of factoring commissions

Let's take a closer look at the principles for determining the main factoring commissions. The amount of commission for monetary resources, which is subject to withholding by the factor upon final settlement with the client on a monetary claim, increases by the amount of VAT at the current tax rate and is determined by the following formula:

D = D + D * 18% (1);

D = Tsnom * PRfin * STpr / 100% * Tpl / 365,

where Tsnom is the nominal amount of the monetary claim (in rubles); PRfin - percentage of financing of a monetary claim (of the amount of the claim); STpp - rate of placement of monetary resources by factor (in percent per annum); Tpl - payment period, i.e. the period of time from the moment of financing of the monetary claim by the factor until the moment of payment of the latter by the debtor, client or third party (in days).

The rate of placement of monetary resources by a factor is set in the currency of the Russian Federation as a percentage per annum of the amount of financing provided by it and is defined as the rate of attraction of monetary resources by the factor, i.e. the cost of the funding it attracts plus the factor margin.

The commission for factoring services is set as a percentage of the amount of monetary claims assigned to the factor; in addition, VAT is charged at the current tax rate. The amount of remuneration is determined based on the value of the following key parameters (Table 2).

The number of debtors whose monetary claims will be assigned to the factor;

The level of risk concentration on debtors, whose monetary claims will be assigned to the factor;

The number of invoices issued by the client to debtors during the month;

Availability of returns of goods from debtors;

Availability of a client's guarantee for debtors' obligations;

Actual geographical location of debtors;

History of trade (business) relationships between the client and debtors.

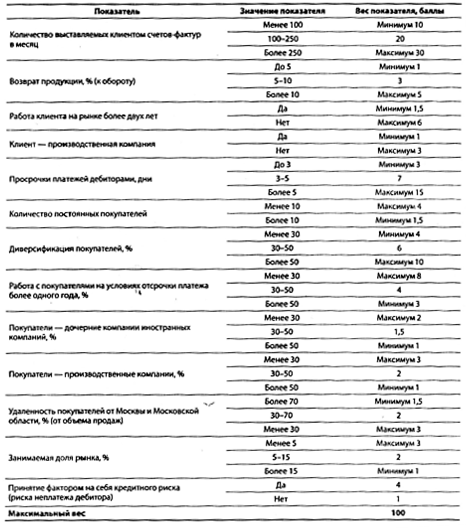

The full set of parameters is presented in table. 2.

The amount of reward is set depending on the number of points scored. An example of calculating points is given in table. 3, rewards - in table. 4. The final result of assessing the client’s key parameters in our case is 33.5 points. Based on the results of an analysis of the client’s key parameters, the amount of remuneration for factoring services can be set in the range from 0.1% to 2% or more of the amount of assigned claims.

The commission fee for document processing is set at 25-75 rubles, in addition, VAT is taken into account at the current tax rate (for one set of documents for one delivery). The amount of this commission is 25-50 rubles. for one set of documents for one delivery for clients classified as large, and 50-75 rubles. for one set of documents for one delivery for clients classified as medium. Classification of clients into certain categories is carried out in accordance with the procedure in force at the factor.

Table 2. Calculation of commission for factoring services

Table 3. Client rating

Table 4. Remuneration calculation

The commission for organizing a transaction is set as a percentage in the amount of 0.05-0.5% of the approved limit for the client’s portfolio, in addition, VAT is taken into account at the current tax rate. Often a minimum amount for this commission is also set.

Thus, when determining the cost of factoring services for clients, various conditions are taken into account: the stability of the position of the client and his debtor, the method of payment under the agreement (for example, a letter of credit and collection have different guarantee values), the time of payment (an existing or future claim), the quantity claims transferred by the client to the financial agent, etc. The amount of remuneration can also be calculated in different ways: in the form of a fixed amount, a percentage of the value of the transferred claims, the difference between the nominal value of the claim specified in the contract and its estimated (actual, market) value.

Since factoring, in accordance with world practice and Russian legislation, is not a credit operation, the factoring commission cannot be calculated as a percentage per annum. Moreover, unlike interest on a bank loan, which is included in the cost in the amount of the discount rate of the Central Bank of the Russian Federation plus 396, the factoring commission, according to the Regulations on the composition of costs for the production and sale of products (works, services), included in the cost... from August 5, 1992 ZR552, fully attributable to cost. It must be borne in mind that only the fee for the provision of monetary resources shows the cost of money for the seller and is therefore charged by the factor as a percentage of the amount of the early payment for each day from the date of payment until the day the corresponding funds arrive in the bank account (but not more than for the period of deferment payment plus 30 days) and therefore can be recalculated as interest per annum.

Typically, the commission schemes of different operators are identical, which indicates blind copying of the experience of the first players, underdevelopment and inexperience of the market. New players often follow the path of price dumping, which negatively affects the development of the factoring services market in the Russian Federation, because the price of a service should reflect its cost and a certain rate of marginal profit, which is laid down by the operator.

It is also important to know how deductions and commissions are collected during factoring services. Repayment of financing against the assignment of a monetary claim is carried out through the receipt and subsequent accounting of debtor payments. Upon receipt of payment from the debtor, the factor, in accordance with the agreement, transfers to the client the remaining amount of financing in accordance with the terms of the agreement minus the factor’s commission, consisting of all commissions, penalties and fines accrued to him under the agreement.

After the factor receives payment from a client, debtor or third party for a specific monetary claim, the factor transfers to the client’s account the cost of the monetary claim minus the financed amount, the amount of commission for monetary resources, for factoring services, processing documents and organizing the transaction. The amount of commission for monetary resources is set as a percentage of the amount of the monetary claim financed by the factor, and is calculated from the date of transfer of financing to the client’s account until the date of receipt from the debtor of payment in full for the claim financed in this way. In the event of partial payment of the claim by the debtor, the amount of the commission for monetary resources will be calculated on the remaining amount of outstanding financing until full payment. In the case of partial repayment of the value of a monetary claim, the amount of commission for monetary resources is calculated based on the amount of the partially repaid claim.

Remuneration for factoring services, for document processing, as well as penalties and fines are withheld by the factor from the amount of the corresponding payment payable to the client after receipt of full or partial payment of the corresponding claim to the factor’s account from the debtor and/or in cases provided for in the financing agreement for the assignment of monetary claims. from the client. If the debtor fails to fulfill the requirement and the factor implements the provisions of the debtor's guarantee agreement, the specified remuneration of the factor is paid by the client in the manner prescribed by these provisions. The above remuneration is retained by the factor as a lump sum as the debtor(s) build payment of financed cash claims. The remuneration for organizing a transaction is set in a fixed amount and is subject to payment by the client to the factor no later than 10 calendar days from the date of signing the contract.

For a final assessment of the impact of factoring on the turnover of receivables, you can also calculate the coefficient of release (additional involvement) of receivables, which will allow you to estimate the amount released as a result of factoring:

K e = (T ob.dz.1 - T ob.dz.0) * Q r / T,

T ob.dz.1, T ob.dz.0 - the duration of one turnover in days in the previous and reporting periods, respectively (after the start of using factoring); Q р - actual volume of products sold in the reporting period; T - number of days in the reporting period.

In addition to the commissions themselves, there are a number of other non-price factors that have a great influence on the client when choosing a factor. Here are the most common of them:

Funding percentage;

Availability and duration of the grace period;

Financing limit size;

Financing based on copies of documents;

Availability of electronic factoring;

Financing of old supplies (supplies that have been made, but the payment period for which has not yet arrived);

Financing term;

The number of documents that must be provided to the factor for each delivery.

The most important of the above criteria is the percentage of funding. Its value affects the cost of factoring services. The percentage of financing is determined separately for each debtor. When determining the percentage of financing, the main importance is the size of possible deductions and direct payments from a given debtor, therefore, at the stage of determining the percentage of financing, an analysis of write-offs and deductions in relation to supplies to a given debtor is carried out:

Pf max = 100% - (V av + 10%), (3)

where Pf max is the maximum percentage of financing from the amount of the requirement; In Wed - the average amount of deductions for the period, %.

The average amount of deductions for the period is calculated as the average amount of credit notes, discounts, returns goods, etc.

After the start of financing the client’s claims to this debtor, write-offs and deductions are monitored on a regular basis to confirm / change the percentage of financing. The indicator “conditions for financing supplies” includes such parameters as the possibility of financing using copies of documents and financing old supplies, the number of documents that must be provided to the factor for each delivery, and the availability of electronic factoring. Other non-price parameters of the factoring company’s activities can be assessed by the client based on publicly available sources of information, such as the factor’s website, ratings of factoring companies, and information in the press.

You should also pay attention to the following circumstance. One of the conditions that ensures the effectiveness of factoring services is that the factor finances all or almost all of the seller's supplies over a long period of time. Only in this case can the seller count on implementing his sales expansion program without fear of a shortage of working capital. This means that in the interim, the factor will be forced to finance the client’s sales, with almost no impact on the selection of counterparties, pricing policy and other significant aspects of its sales strategy. In order to avoid the threats associated with this situation, factoring companies do not pay advance payments in full after delivery (usually 60-90%). This retains the seller’s interest in pursuing an optimal sales policy taking into account the market situation, since, By preventing the occurrence of additional losses of the factor, the seller thereby protects himself from losses.

Additional income and benefits of the supplier associated with factoring services:

1. Obtaining additional profit due to the opportunity to increase sales volume by receiving the necessary working capital from the factor;

2. Obtaining additional profit from an increase in turnover due to a decrease in the price of products sold and an increase in the term of commodity lending, i.e. additional competitive advantages;

3. Savings due to the opportunity to purchase goods from your suppliers at lower prices. This opportunity arises due to the fact that the client, receiving a significant part of the delivery amount on the delivery day, and thereby losing dependence on the observance of payment discipline by its debtors, can shorten the deferred payment period when purchasing goods and demand better prices from its suppliers conditions for the purchased goods. In addition, he receives a guarantee of protection from penalties from creditors in case of untimely settlements with them caused by a cash gap;

Protection against losses due to non-payment or late payment by debtors for goods delivered to them. Especially when using two-stage factoring;

Savings on paying for additional places (including office equipment) and additional working time for employees;

Protection against lost profits from loss of customers due to the inability to provide customers with competitive deferred payments and maintain a sufficient range of goods in stock if there is a shortage of working capital.

Additional income when using factoring, as well as when receiving additional profit due to the opportunity to increase sales volume, will be equal to:

DD = Rp*SP + DF*SP*Kvp/s – Z (10)

where Рп – profitability of sales;

SP – delivery amount;

DF – amount of financing for factoring in shares;

KVP/s is a coefficient reflecting the ratio of gross profit to cost of goods sold. In this formula, it is advisable to use this coefficient, and not the return on sales. Because the receipt of an advance payment for factoring is not yet our income, but will become such after we purchase a new batch of goods and deliver it to the client;

Z – factoring costs.

Since the amount of supplies for 90 days is equal to 1500 thousand rubles, the additional income for 3 months will be equal to:

DD = 30.3%*1500 thousand rubles. +90%*1500 thousand rubles*(13124 thousand rubles/285371 thousand rubles) – 68880 rubles. = 448 thousand rubles.

Therefore, the additional income when using factoring for the year will be equal to:

DD = 448 thousand rubles * 4 = 1792 thousand rubles.

Factoring costs, as previously calculated, will amount to 68,880 rubles. = 69 thousand rubles. Consequently, income exceeds expenses. Thus, we can draw a conclusion about the feasibility and effectiveness of factoring.

The efficiency of capital use is characterized by its profitability (profitability).

By planning overall profitability, the required level of production efficiency for the coming period is established and the actual use of funds is monitored. In general, for industry, the level of overall profitability is determined based not only on the amount of profit received, but also on the entire amount of net income, i.e. the total amount of cash savings (profit, turnover tax, other cash savings).

The profitability indicator is used to assess the economic and financial activities of enterprises (associations) and is one of the elements of a unified system of economic incentives.

Let's calculate new profitability indicators.

Total return on capital is equal to the ratio of balance sheet profit to the average value of the entire property of the enterprise for the reporting period:

Balance sheet profit = 7617+1792 = 9409 thousand rubles.

Overall profitability = 9409/0.5*(211672+217949) = 0.0438.

This means that the company will receive 4.38 rubles. profit per ruble of invested capital.

CHAPTER 3. EVALUATION OF THE EFFICIENCY OF THE BANK'S FACTORING SERVICES

3.1. Calculation of the cost of factoring services

In the context of the constant expansion of the market for factoring services and increasing competition, in order to strengthen and maintain their positions, factoring divisions of banks (factoring companies) offer their clients an ever-increasing list of banking products, improve the quality of their provision, that is, the marketing approach comes to the forefront in the activities of factoring management, focused on the needs of potential buyers.

Of particular importance in such a situation is an effective pricing policy and factor strategy, which should ensure the profitability and profitability of its operations. There are various pricing methods and strategies, however, the price of a factoring product is based on its cost, the determination of which for a factor is one of the most pressing problems.

In order to offer the best price to the client, and at the same time not offend himself, the factor needs to have a good understanding of the structure of his costs, the list of services, have a tool for calculating the cost of each product, and also clearly understand which departments and employees are involved in the business process when providing this or that services.

In view of the fact that factoring includes a complex of services and operations, and in banking marketing these concepts are not identical, the author considers it necessary to consider the cost of operations performed by employees in the process of factoring services and the cost of services that the factoring management sells to its clients as part of the factoring product .

The cost of a factoring product consists of three commissions:

Financing fees;

Commissions for factoring services;

Document processing fees.

The main components that form the interest rate and financing fee are:

Funding cost,

Margin for accepting risk,

Cost of capital (reserves).

The financing fee is calculated as a percentage for each day of use of the provided funds and is charged at the time of receipt of funds to pay for the delivery.

The cost of funding is the cost of resources attracted by a factor to carry out its activities.

When accepting a client for factoring services, the factor also assumes risks: the risk of late payment for delivery, insolvency of the debtor, sharp changes in the cost of credit resources, bankruptcy and fraud of the seller. Accordingly, factors in the financing fee include the risk premium. However, the margin for accepting risk by a factor is set individually and depends on:

Client's financial condition;

Number of debtors;

Qualities of debtors, i.e. quality of payment discipline and financial condition of the debtor.

Factoring financing is usually characterized by credit management of debtors, including:

Checking debtors, their solvency and setting limits;

Verification of supplies;

Control;

Collection functions.

All these services are compensated by a commission for factoring services, which is usually charged as a certain percentage of the entire amount of the assigned monetary claim; this premium is accrued at the time of financing the client, and is charged at the time of receipt of funds to pay for the delivery.

Since the amount of this commission directly depends on the turnover, the percentage value is tied to the turnover. That is, the greater the turnover and the number of debtors transferred by the client for factoring services, the lower the percentage of the commission charged.

Factoring involves a lot of paperwork. Checking and processing shipping documents is an integral part of the factor's daily work. These labor costs are compensated by the factor by charging a commission in the form of a fixed fee for a set of documents.

To calculate the cost of the operation for processing shipping documents, two parameters need to be determined:

Labor cost per unit;

The time it takes to complete a particular operation.

To determine the cost of a unit of labor, the total costs associated with maintaining a particular division of the company and the practical number of working hours that can be used to create a product or provide a client service are used. The practical number of hours differs from the actual number of working hours based on the fact that the employee spends 80–90% of the total time spent at the workplace performing work. Thus, knowing the cost per unit of time and the time required to produce one product, you can obtain the cost of the product being manufactured.

A customer service department specialist checks and processes shipping documents. Let’s assume that the total cost of maintaining this department is 20,000,000 rubles per year, and the department employs 20 people.

On the one hand, the cost of working time for a department employee consists of his salary, maintenance of the premises and other expenses associated with him personally. On the other hand, the department incurs additional costs that are not related to the employee in question. Since the productivity of the branch directly depends on the number of employees directly involved in servicing clients, when calculating the cost of services the author will take into account the total costs of the bank branch. The cost of a working hour is calculated using the following formula:

Where  - cost of working hour

- cost of working hour

E- costs of maintaining a factoring unit per year, including personnel costs, maintenance of real estate, computer equipment, business expenses

N – number of department employees

256 – number of working days in a year

8 – number of working hours per day

Having carried out the calculations, it turns out that in the example under consideration, the cost of a working hour for an employee involved in document processing averages 610.35 rubles (200,00000/20/256/6.4).

Then it is necessary to determine the time required to carry out a particular operation. For this purpose, direct measurements of the time spent by department employees on processing shipping documents are carried out. Thus, the cost of the operation for processing shipping documents is calculated using the following formula:

Ci=CT(i)*Ct , (2)

Where C.T.(i) – time to complete an operation in man-hours, obtained by measurements at employee workplaces.

The document processing fee consists of the cost of two operations, namely: checking the correctness of the application for financing, the acceptance certificate, the invoice, the waybill and other documents related to the shipment, as well as the processing of shipping documents, i.e. reflected in the automated factoring operations management system. An employee spends an average of 2 minutes on the first operation; an employee spends an average of 1 minute on registering 1 waybill and invoice; therefore, an employee spends 3 minutes processing 1 set of documents for one shipment. Thus, the cost of factoring management for processing shipping documents is 30.52 rubles (610.35/60*3).

To calculate the cost of factoring services, it is necessary to classify the costs associated with the implementation of factoring activities. All factor expenses can be divided into two groups: operating and non-operating, which in turn are divided into circulating taxes and expenses for attracting financial resources on the one hand, and current expenses and capital investments on the other. Current expenses consist of expenses for the maintenance of the apparatus, business expenses, expenses for the maintenance of fixed assets, transportation expenses, expenses for IT (software and technology), expenses for information and consulting services, as well as commercial expenses.

First, you need to decide on a complete list of services in the field of factoring. As mentioned above, factoring includes financing, administrative management, information and analytical services. It is advisable to consider the degree of participation of factoring units in the provision of the listed range of services.

Financing is handled by specialists from the customer service department. The operation itself is carried out on the basis of registered shipping documents provided by the client for deliveries made in favor of its counterparties (debtors). In addition, customer service is involved in maintaining statistics on debtors and clients. Specialists of the credit control department are directly involved in the provision of this service, who monitor the conduct of transactions within the framework of the methodology for setting limits; permissive and prohibitive operations within the framework of financing; advising the client on the emergence of risks in the field of trading with deferred payment. The attraction department conducts negotiations with clients and employees of structural divisions within the bank, draws up, agrees with the client and signs the general agreement, additional agreements to the general agreement; develops, edits, and coordinates factoring documentation. The Methodology and Business Development Department is engaged in the development, execution, coordination of rules for carrying out operations, additional agreements to the General Agreement; carries out control, reconciliation of reports, development and editing of documentation on factoring. In addition, the methodology and business development department is engaged in the development of new products and services, non-standard factoring service schemes aimed at meeting the diverse needs of clients. The department for support and implementation of factoring technologies carries out computer implementation of new products and services, non-standard factoring service schemes, develops and ensures the operation of the software module necessary for the effective implementation of activities.

The administrative management of client receivables is carried out by several departments, namely: the customer service department and the credit control and risk management department. Specialists of the customer service department carry out administrative management within the framework of the general agreement and additional agreement to the general agreement and supply agreement, in terms of assessing the quality of the client's receivables by classifying the current delay in payment for the client's supplies by debtors, in addition, they remind the debtor about the due date of payment for the delivery. The credit control department carries out administrative management of the client's receivables for recourse deliveries, direct payments and returns in the event of critical and negative debt; advising the client on the emergence of risks in the field of trading with deferred payment; establishing recommended shipment limits for the client. If a delay occurs, it is important to inform the client about this in time, find out why this happened, and take the necessary measures to resolve the misunderstanding. Indeed, due to long and constant delays, the client’s risk group regarding an unreliable debtor may increase, which may lead to a refusal to further finance supplies made by the client in favor of this debtor.

Information and analytical support for the Client’s activities is carried out with the participation of the following business units. The department for support and implementation of factoring technologies is engaged in the development and development of software and the installation of a client module. At the beginning of the month, the customer service department generates reports for the client on the status of accounts receivable, volumes of financing, registration of supplies, written off commissions, in addition, advises clients on accrued and written off commissions, and the correct execution of documents. The Department of Methodology and Regional Development, within the framework of information and analytical support, is engaged in the development of service schemes, new products and services, preparation of materials for the website, preparation and publication of articles on factoring.

Based on the grouping of services by departments directly involved in factoring services, it is possible to calculate the cost of factoring services for one delivery based on labor costs.

The total cost of maintaining the bank's factoring management per year is 327,465,000 rubles (according to the balance sheet and profit and loss report, Appendix 7). The number of personnel is 200 people. Substituting the data into formula 1, we find that the cost of one working hour is 999.34 rubles. The total number of minutes spent on servicing one delivery is on average 220 minutes. Having made calculations using formula 2, it turns out that the cost of managing the bank’s factoring operations for providing services for one customer delivery under the factoring agreement is 3,664.26 rubles. However, do not forget that this calculation is based only on labor costs and does not take into account the cost of money; in addition, when calculating the cost of servicing subsequent deliveries, the cost of labor costs will be less. This is based on the fact that only when servicing the first delivery of a client, all departments are involved in this process, ranging from labor costs to attract a client, collecting the necessary documentation, approving limits, checking documentation, creating a client dossier, registering deliveries, verification, financing and monitoring. Subsequent servicing is based on the received data, the generated client dossier, established relationships with the contact person of the client and debtor, and, therefore, requires less time to carry out and fewer people involved.

Let's consider an algorithm for calculating the cost of factoring operations, which allows us to analyze the cost of servicing customer invoices when carrying out factoring operations, as well as identify the ratio of operating costs in order to correlate them with the level of commission directly for a given client 30.

Initially, the total number of recorded deliveries for the costing period is determined. For convenience, we set the calculation period to 1 month. Let's say that during this period the customer service department recorded 15,000 deliveries.

The next step is to determine the total cost, which is determined by the algebraic addition of operating expenses and non-operating expenses for the calculation period. The total cost of the factoring management under consideration is 46,182,083.33 rubles (according to the balance sheet and income statement, Appendix 7), adjusted to the average value of the calculation period).

The cost of factoring services for one delivery is determined by the following formula:

Cost of one delivery = Ps/Pk, (3)

where Pk is the total number of registered deliveries

Having made the calculations, it turns out that the cost of factoring services for one delivery is 3078.81 rubles.

In general, the cost of factoring consists of the following components:

Cost of money (usually from 7 to 16% per annum);

Expenses not related to changes in the value of money (from 0.2 to 5%);

The risk premium associated with possible losses is set by the bank independently, based on internal rules (from 0.5 to 12%);

Profit factor (from 2%).

The cost of factoring services is different for each client. It depends on the industry in which the client operates, the size of his business, the quality of receivables, the deferment period, turnover, and the range of services chosen.

In the current Russian conditions, factoring with recourse is most in demand, due to its relatively low cost compared to non-recourse factoring. But for the factor, the most profitable, however, and riskier product is non-recourse factoring. The risk premium in a non-recourse product is close to the maximum value, however, in the case of a positive outcome of the operation, namely timely and full repayment of the delivery, the factor’s profit is significant. A comparison of the profit margin and factoring management risk premium for factoring with and without recourse is shown in Diagrams 2 and 3 (Appendix 8).

3.2. Profitability of bank factoring operations

The efficiency of a bank's factoring department is determined by the profitability of its operations and its ability to maximize profits while maintaining the required level of risk. Profitability reflects the positive overall result of the bank's factoring management.

Profit is the main indicator of business performance. The difference between income and expenses is gross profit. In a general economic sense, the concepts of profitability and profitability coincide. Therefore, it is actually necessary to calculate the profitability indicator of the bank's factoring department.

Profitability characterizes the level of return per 1 ruble of invested funds, which in relation to the bank's factoring department means the ratio of the amount of profit received and funds contributed by the bank's shareholders.

To analyze the bank's factoring activities, it is proposed to use the following indicators:

Amounts transferred by the bank to suppliers;

Amounts reimbursed by payers to the bank;

Amounts not reimbursed by payers to the bank;

Income from factoring operations;

Document processing fee;

Accounts receivable management fee;

Interest on financing accrued on the daily balance of the advance paid to the client.

The analysis of the considered indicators should be carried out in dynamics by comparing the reporting data with similar indicators for previous dates. This comparison will make it possible to find out trends in the development of factoring services in the bank and take the necessary measures if negative trends are identified.

An analysis of the individual indicators listed above is presented in Table 1; the calculation was made based on data from the National Factoring Company bank.

Table 1

Interest income on factoring operations, thousand rubles.

RATES OF GROWTH, % | GROWTH RATE, % |

|||

ACCOUNTS RECEIVABLE FINANCING | ||||

ACCOUNTS RECEIVABLES SERVICE | ||||

RISK PREMIUM |

The data obtained indicate an increase in the number of companies served, an increase in financing volumes, and, as a result, an increase in the factor’s income. A significant increase in the risk premium indicates both the attraction of riskier clients for servicing and an increase in the percentage of non-recourse factoring in the bank’s portfolio, and, consequently, an increase in profits.

To assess the effectiveness of factoring activities, there is the following system of indicators:

analysis of the effectiveness of a factoring transaction:

Profitability of a factoring transaction;

The employee’s performance during a factoring transaction;

2) analysis of the profitability of factoring operations of a bank division:

Profitability of the factoring division;

The ratio of the factoring division's profit to the average value of the assets required to obtain it.

The profitability of a factoring transaction is determined through the ratio of transaction income to transaction costs. For one transaction, the factor received income in the amount of 25,000 rubles; expenses in the amount of 10,000 rubles were incurred to carry out this transaction. Therefore, the profitability of a factoring transaction is 2.5 (or 250%).

The efficiency of employees is determined by dividing the factoring division's profit from a transaction by the number of employees involved in the transaction. Based on the example under consideration, the profit from the transaction is 15,000 rubles, 10 people take part in one transaction, therefore, the employee’s work efficiency is 1,500.

The profitability of a factoring division is defined as the ratio of the profit received to the expenses of the factoring division.

According to the balance sheet and profit and loss report (Appendix 7), the profitability of the factoring division of the bank in question is 72.64% (402583000/554185000*100%), which undoubtedly indicates the efficiency of the division.

Assessing the effectiveness of a factoring business is based on qualitative and quantitative indicators.

Qualitative indicators of the Factor’s performance include:

Complete implementation of the main tasks and functions of structural units;

Compliance by employees with established work technologies;

The pace of employee promotion;

Product range development;

The expansion of the customer base;

Optimization of business processes and technological improvement of business.

Quantitative indicators are characterized by:

Dynamics of turnover;

Dynamics of the number of debtors;

Dynamics of the number of clients;

Dynamics of the number of supplies;

Dynamics of the profit received.

The effectiveness of factoring operations for a factor can be determined using a three-stage assessment system 31, which is based on formulas for calculating the turnover of assets and receivables, as well as calculating the weighted average profitability of a factoring operation.

The factoring company's asset turnover formula (4) allows you to plan the company's cash flows over time, since it takes into account the influx of cash in the form of repayment of financing.

, (4)

, (4)

Where  - asset turnover during the period

- asset turnover during the period

n– number of financing repayments

- amount of separate financing repayment

- amount of separate financing repayment

D - date of financing

- date of financing

D - financing repayment date

- financing repayment date

Using the receivables turnover formula (5), you can evaluate the efficiency of organizing the factor’s work with its clients and the quality of the client portfolio. It can serve as an indicator for determining the pricing policy of the factor in terms of establishing the amount of commissions for factoring services.

, (5)

, (5)

Where  - accounts receivable turnover in the period

- accounts receivable turnover in the period

pl- number of debtor payments during the period

- the amount of a separate payment by the debtor

- the amount of a separate payment by the debtor

D - debtor payment date

- debtor payment date

D - date of delivery.

- date of delivery.

The factoring operation profitability formula (6) allows you to calculate the margin on factoring operations, as well as evaluate the overall activity of the factor from the point of view of economic efficiency. The obtained values can serve as reliable information for owners and shareholders, and can also be used to assess the value of a company's business in the event of a reorganization, merger or acquisition.

, (6)

, (6)

Where  - profitability of factoring operation

- profitability of factoring operation

- the amount of the factor’s commission received from each repayment of financing

- the amount of the factor’s commission received from each repayment of financing

D- date of financing

D- financing repayment date.

Let's carry out calculations using the above formulas. Let's set the calculation period to 1 day. Let us consider for comparison 2 days, the data for which is reflected in Appendix 10. Asset turnover for April 25 is 46.35, while for April 24 the asset turnover was 54.13. If we assume that the amounts of individual repayment of financing are equal to the amounts of payments of debtors (which indicates the timeliness and completeness of fulfillment of obligations), then the asset turnover is equal to the receivables turnover.

Based on the initial data, calculations were made for the commissions due to the factor, based on the tariff sheet (Appendix 9), the data is presented in tables 2 and 3 (Appendix 10). Based on the results obtained and making calculations using formula 6, we can conclude that the average profitability of factoring operations exceeds 29.6% per annum.

If you carry out calculations by month throughout the year, you can notice the seasonality of demand for factoring services. Factoring is most in demand in the fall and December, this is explained by the desire of clients to close the year with minimal receivables. January and summer months are characterized by low demand, due to the decrease in business activity caused by the New Year holidays and the vacation period.

CONCLUSION

Factoring, unlike traditional financial businesses, is an innovative branch of the economy that most closely meets the needs of suppliers of the 21st century, namely: building a profitable business in conditions of highly competitive markets and the “dictation” of the buyer.

The effectiveness of any business primarily depends on the competent organization of business processes, clearly defining the responsibilities and powers of employees, developing policies, and internal regulations. This is especially true for the factoring business, due to its unsecured and complex nature, because in addition to the financing itself, it includes credit risk insurance, accounts receivable management, as well as its examination, monitoring and collection activities.

The main goal of the work was to analyze the effectiveness of the bank's factoring operations, determine the factors influencing the activities of the factoring division and ways to minimize and restructure them.

Based on the work done, we can conclude that the three most important components of the factoring business, which ensure customer loyalty and, as a result, success in the factoring market and operational efficiency, are:

High quality software. Factoring services are a high-tech business. To ensure uninterrupted and high-quality customer service, the factor must have a set of information systems that ensure the automation of all basic business processes;

Effective risk management tailored to the specifics of factoring. The only guarantee of financing in factoring is high-quality, valid, verified receivables for assigned monetary claims, therefore the successful operation of a factoring company is impossible without competent assessment and management of risks arising during factoring operations. By assessing all participants in the transaction, analyzing the relationship, including contractual ones, between the supplier and the debtor, analyzing the goods supplied by the supplier, taking into account information on the industries in which the debtor and supplier operate, the factoring company can fully assess the emerging when factoring services there are risks and try to minimize the level of these risks;

Staff of professional employees.

In the process of increasing competition, optimization of pricing policy is becoming increasingly important, so it is important for a factor to understand what the cost of its product consists of. In view of the analysis, we can conclude that the factor forms the cost of its services based on four components:

Cost of money;

Risk premium;

Expenses not related to the value of money;

Desired profit.

In turn, for the client, the cost of factoring services depends on the size of his business, the quality of receivables, the industry in which he operates, the deferment period, the set of selected services and the type of factoring.

To fully disclose the set goal, the cost of factoring operations was calculated not only on the basis of the cash costs required to carry out the activity, but also from the point of view of the labor costs expended by employees in the process of factoring services.

Undoubtedly, launching a factoring service requires enormous costs from the bank - both time and financial. To build a factoring division, establish mechanisms and technologies for conducting operations, it takes an average of 8 months to 1 year. The factoring business will not pay for itself in a couple of months, but its prospects and profitability are beyond doubt. Based on the calculations carried out, we can talk about the high profitability and efficiency of factoring operations, both for the factor itself and for its clients, because factoring allows the latter to increase turnover, sales volume, eliminate cash gaps, increase their competitive position, and expand the circle of debtors.

BIBLIOGRAPHY

1 Factoring: Modern American Style/ Presented for the World Bank, () presentation

2 Pokamestov I.E. Factoring: Textbook, guide to studying the discipline, workshop - M.: MESI, 2004

25 Kozhina L.M., Construction of an optimal technology for carrying out factoring operations, “Factoring and trade finance”, No. 1/2008, 2008

26 (list of documents for an application for factoring services)

27 a set of measures aimed at identifying invalid accounts receivable, as well as other factors preventing the parties from conscientiously fulfilling their obligations under the contract. Encyclopedia Factoring Market Expertise, - RA Expert May 2008

28 Olga Grishina, Risk management and factoring, – Russian factoring market in the first half of 2006. Rating agency "Expert RA"

29 /research/factor/

30 Pokamestov I. E. Dissertation for the academic degree of Candidate of Economic Sciences, “Effective organization of factoring business”, 2007

31 Pokamestov I. E. Dissertation for the academic degree of Candidate of Economic Sciences, “Effective organization of factoring business”, 2007

Graduation qualifyingJob consists of an introduction, three...

The final qualifying work is a complex document

TextbooksGraduationqualifyingJob is a complex document in which the applicant... in the form of tables, which is acceptable for graduationworks with a special question on purely technical matters...

GRADUATIONQUALIFICATIONJOB on the topic: “Legal regulation... ….So, the purpose of this thesis work– explore possible ways of improvement... …. ….Relevance of the chosen thesis topic work due to the fact that legal regulation...

GraduationqualifyingJob

(1 ratings, on average: 5,00 out of 5)

(1 ratings, on average: 5,00 out of 5)